“Private companies are a critical part of the global economy and through private equity, investors can access this vast opportunity set.”

~ Steve Schwarzman, Chairman, CEO & Co-Founder of Blackstone

Private companies are staying private longer, shifting more of the growth opportunity set outside public markets and making private market access increasingly important for diversified investors.

The IPO market is reopening selectively, with investors favoring durable business models, profitability visibility, and disciplined valuations over speculative growth narratives.

Large potential listings such as SpaceX or Anthropic could meaningfully affect market leadership, index composition, and investor sentiment, but fundamentals, valuation, and risk management remain essential.

Ignoring private markets eliminates a meaningful portion of the investable universe, whereas incorporating the private opportunity set can offer enhanced diversification and other benefits.

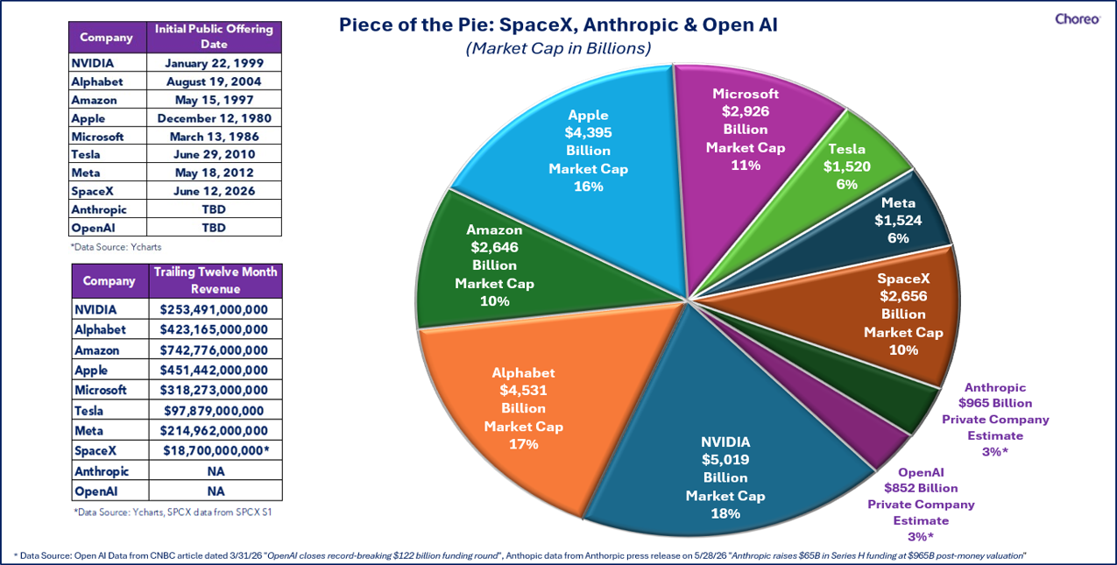

A unicorn is a mythical creature born of imagination. In the investment world, the term describes a private company valued at $1 billion or more—large enough to capture public attention, yet still largely inaccessible to most public-market investors. On June 12, 2026, the largest initial public offering (“IPO”) in history occurred when SpaceX, Elon Musk’s space exploration and technology company, began trading publicly. The debut placed SpaceX’s public-market valuation near $1.8 trillion, making it one of the largest companies in the United States. SpaceX may be the ultimate unicorn, but it is not alone. Several other high-profile private companies, including Anthropic and OpenAI, are expected to consider public listings in the not-too-distant future.

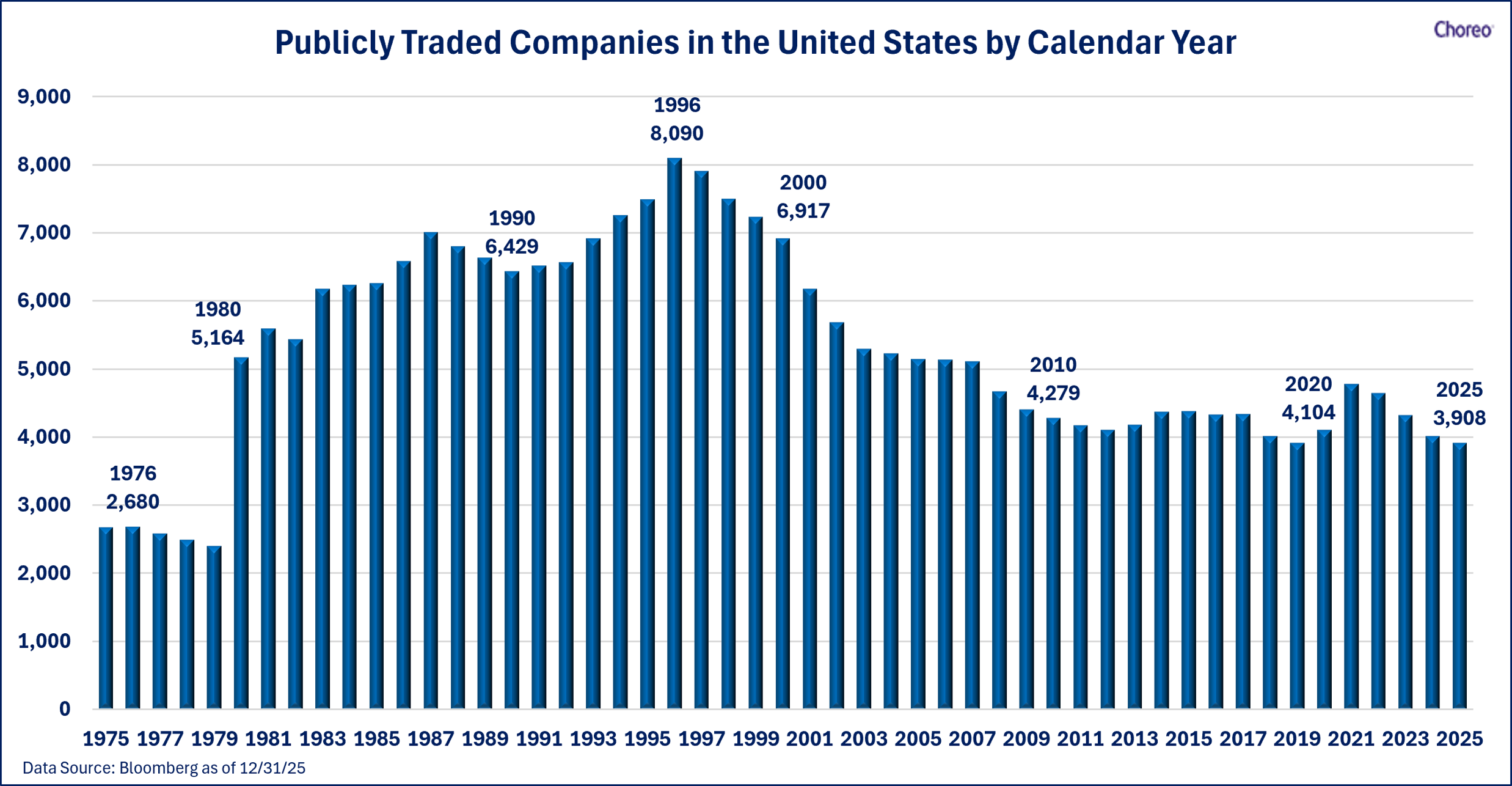

Companies now have greater access to private capital—including venture capital, private equity, and other institutional sources—which allows them to scale without immediately turning to public markets. At the same time, employees and early investors have gained more access to pre-IPO liquidity, reducing the pressure for companies to list earlier. As a result, firms are generally remaining private longer, and growing for longer, allowing for more unicorn sightings. Many companies are waiting 12–14 years before going public, nearly twice as long as companies did in the 1990s . The number of publicly traded companies has also shrunk over time as shown in the graph below, meaning that if private markets are ignored, an investor is ignoring a meaningful portion of the investable universe. Even so, going public remains an important milestone for many companies because it can provide access to a larger and more permanent pool of capital, create a strategic currency for acquisitions and compensation, and offer liquidity for early stakeholders.

IPO Market: A Gradual Reopening

After a subdued start to the year, the IPO market is showing signs of reawakening, but the recovery remains uneven and highly selective. Investors are rewarding companies with clear paths to profitability, disciplined capital allocation, and business models that can withstand higher-for-longer interest rates. Companies with distinctive competitive advantages and long runways for growth, such as SpaceX, have also attracted strong demand. By contrast, issuers that rely too heavily on distant growth narratives or cheap capital are finding that the window is only partially open.

The pipeline is building across technology, healthcare, and consumer names, but deal outcomes are increasingly bifurcated. High-quality issuers with established revenues and strong cash-flow visibility are pricing toward the upper end of ranges and trading relatively well in the aftermarket. Others are being forced to cut valuations, reduce deal sizes, or postpone offerings altogether. This dynamic underscores a key theme for 2026: the IPO market is no longer a rising tide that lifts all boats. Instead, it has become a sorting mechanism that distinguishes companies with durable business models from speculative stories.

Macro conditions remain a critical swing factor. Elevated policy rates, tighter financial conditions, and lingering inflation uncertainty have raised the bar for both issuers and investors. At the same time, resilient labor markets and steady economic growth have supported risk appetite enough to keep the IPO window from closing outright.

For long-term investors, the IPO itself is typically less important than what comes after. Many attractive opportunities may emerge not on day one, but after [RM1.1]any initial volatility has subsided, and companies have reported for a few quarters as public entities. Broadly diversified portfolios will generally gain exposure to newly public companies over time once those companies meet the requirements for index inclusion.

Don’t Ignore Private Markets

The factors above point to an obvious subtext: private markets remain an increasingly important part of the long-term opportunity set for qualified investors. Access has broadened through lower minimums, more flexible structures, and a wider range of strategies. The opportunity extends well beyond the latest high-profile IPO and includes a broad set of companies, asset classes, and risk/return profiles.

There are several reasons an increasing number of investors are allocating capital to private markets. First, as stated above, many of the most dynamic companies stay private longer, or may never go public, which means some of their strongest growth phases may occur outside public markets. Second, private markets can provide access to areas of the economy that are less represented in public benchmarks, including venture-backed innovation, private credit, and specialized real assets. Third, private investments may enhance portfolio diversification when used thoughtfully. Finally, private-market managers often have more influence over company outcomes through governance, strategic support, and operational involvement than typical public-market investors. There are several other reasons private markets are appealing, but these potential benefits do not eliminate the tradeoffs: private investments are generally less liquid, can be more complex, and require careful manager selection. It does, however, help explain why the opportunity set has become too large to ignore.

What History Tells Us

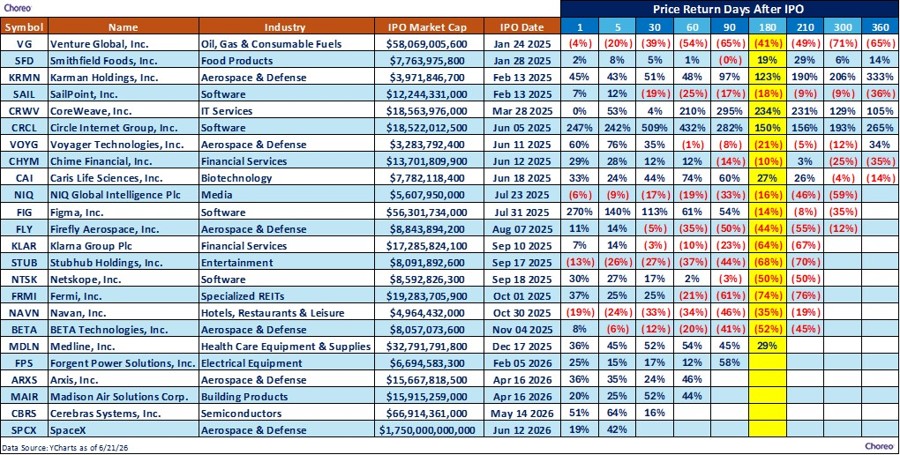

History offers two useful reminders. First, even the most anticipated IPOs rarely move in a straight line after listing. Some ultimately become market leaders, but many experience meaningful volatility as investors digest valuation, earnings quality, lockup expirations, and the transition from private expectations to public-market scrutiny. Second, index inclusion usually takes time. Most newly public companies must first satisfy seasoning, float, profitability, and other eligibility requirements before they can enter major benchmarks, which means their influence on passive portfolios often builds gradually rather than immediately. That is what could make mega-listings such as SpaceX or Anthropic so unusual: if they come public at extraordinary scale, the path from private-market legend to meaningful public-market weight could be much shorter than history would normally suggest. Past IPOs are a reminder that excitement alone is not enough—but size, liquidity, and timing can make certain debuts far more impactful than the average new issue.

A sample of recent IPOs shows that performance can vary widely on day one, day five, and even 180 days after listing. Outcomes depend on valuation, market conditions, lockup dynamics, investor positioning, and the company’s ability to demonstrate durable growth after becoming public.

Impact on Equity Markets

With SpaceX now trading at a valuation north of $2 trillion as of June 16, 2026, it either already is or will likely become one of the largest components of major equity indexes. Anthropic and OpenAI are also expected to command valuations that could place them among the largest companies in the S&P 500 if they eventually list publicly. The emergence of newly public companies of this magnitude could extend well beyond the IPO market. These companies could quickly influence index composition, sector weights, and passive fund flows, while also testing investor appetite for long-duration growth stories in a market already concentrated in a handful of technology leaders. Strong debuts could reinforce enthusiasm around innovation, artificial intelligence, and next-generation infrastructure. Weak debuts, by contrast, would be a reminder that even exceptional private companies must meet public-market demands for transparency, execution, durable cash flow, and disciplined growth. These IPOs may matter as much for what they signal as for their size: whether the next leg of the bull market broadens, or whether capital remains concentrated in the same familiar winners. In the meantime, private markets remain robust and a source of opportunity for long-term investors.

Closing

For investors, this reinforces the need for a broader toolkit and a more flexible mindset. The lines between public and private markets are becoming increasingly blurred, and opportunities—and risks—are distributed across both. Increased access to private capital means public markets are no longer the only place for large companies to exist, and private markets have become a unique path for investor diversification. Navigating this landscape requires discipline, selectivity, and a long-term perspective rather than chasing headlines or timing individual events. Whether through deliberate allocations to private strategies, public-market exposure, or both, the objective remains the same: capture durable growth while managing risk. In a world where today’s unicorns can reshape tomorrow’s market leadership, staying diversified, patient, and grounded in fundamentals will be essential to turning innovation into lasting returns. As always, please reach out to your Choreo advisors with any questions.

Important Disclosures

Opinions are as of the date referenced and are based on sources considered reasonable by Choreo. Opinions are subject to change based on market or economic conditions. There is no guarantee that any of these expectations will become actual results.

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Past performance does not indicate future performance. The indices discussed are unmanaged and do not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, insurance, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. Information has been obtained from a variety of sources believed to be reliable though not independently verified. Choreo, LLC, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services. This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed. Past performance does not indicate future performance. The sole purpose of this document is to inform, and it is not intended to be an offer or solicitation to purchase or sell any security, or investment or service. Investments mentioned in this document may not be suitable for investors. Before making any investment, each investor should carefully consider the risks associated with the investment and make a determination based on the investor’s own particular circumstances, that the investment is consistent with the investor’s investment objectives.

All registered trademarks are intellectual property of Choreo, LLC. © 2026 Choreo, LLC. All Rights Reserved.